As widely expected, the Bank of Japan unanimously kept its policy rate at 0.5%. Governor Kazuo Ueda emphasised the data-dependent nature of the policy decision, but a notable upward revision to the inflation outlook increases the likelihood of a rate hike in October.

BoJ pauses to evaluate how the trade deal will impact the economy and inflation

Markets had widely anticipated there would be no policy action from the Bank of Japan, and also expected upward revisions to CPI forecasts in its quarterly outlook report.

Despite the recent US-Japan tariff agreement, the BoJ will need to take time to evaluate its impact on growth and inflation before adjusting its policy rate, especially given fiscal policy uncertainty. Thus, today’s pause came as no surprise.

In our view, the BoJ has eased its concerns about trade uncertainty and will now focus on the inflation mandate instead of risk management.

GDP forecast remains steady while inflation forecast rises

While it is still too early to gauge the economic impact of the trade deal, the Bank of Japan’s assessment did not appear particularly negative.

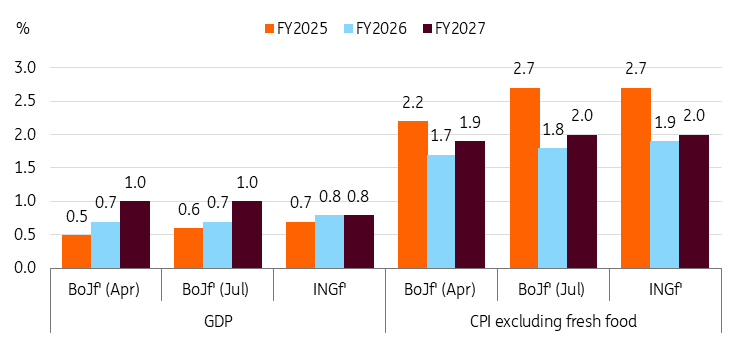

The BoJ highlighted significant downside growth risks but raised its FY25 GDP forecast from 0.5% to 0.6%. Although 1Q25 growth was weak, the BoJ appears to view the economy as continuing to recover as trade uncertainty recedes. The central bank also kept the outlook for FY26 and FY27 unchanged at 0.7% and 1.0% growth, respectively, with the BoJ believing no structural damage will be caused by the tariffs.

Concerning inflation, upward revisions were anticipated due to recent increases in food and service prices. However, the adjustment for FY25 (core inflation from 2.3% to 2.8%) exceeded expectations, and the revised FY26 and FY27 outlook indicates that the Bank of Japan is increasingly convinced that underlying inflationary pressures are persisting.

BoJ revises up inflation and GDP outlook for FY2025

Source: Source: CEIC, ING

A surprise rebound in June activity data supports the BoJ’s steady growth outlook

Industrial production recorded an unexpected rebound of 1.7% MoM seasonally adjusted in June, beating the market consensus of -0.8%. This increase more than offset the previous month’s decline of -0.1%. Output in semiconductor-related sectors posted solid growth, driven by robust investment in AI, while transportation excluding automobiles also showed notable gains.

Additionally, retail sales rose 1.0% in June (compared to -0.6% in May and a market consensus of 0.5%), with the increase being broad-based except for a decrease in fuel sales. Apparel sales grew for the fifth consecutive month, and general merchandise registered its second monthly gain.

With this strong recovery in economic activity in June, we have revised up the 2Q25 GDP forecast to 0.1% QoQ sa from 0.0%. While the pace of recovery remains moderate, the negative effects of tariffs may prove less severe than previously anticipated.

Uncertainty surrounding domestic politics should be closely watched

With the LDP and Komeito coalition recently losing the election, there have been growing concerns over Japan’s fiscal condition. For now, Prime Minister Shigeru Ishiba remains in office, so immediate concerns seem to have been contained.

We expect the cash transfer programme to be executed in the autumn. This would boost private consumption temporarily at least. However, eventually Ishiba will resign and there should be more policy coordination required with opposition parties. As opposition parties advocated for consumption tax cuts, this will keep JGBs under pressure.